There are tons of search engines out there that help you find used cars. Only some sites sell their own vehicles, there are many sites that simply aggregate from these sources. Some are a mix of both where they offer “classified ads” (i.e. private sellers) and aggregates.

The goal of this post is to illustrate many of the different search engines and where they get their results from.

Overview

Here is an overview of all the search engines I’ve come across while researching a relatively new (less than 10 years old) new car.

Autotempest – This is an aggregator of aggregators, designed to help you find the most cars from the most sources in one place. I often start a search here to get a good view of the broad ranges of prices for my desired make and model, year and mileage.

They indicate they aggregate results from ebay, cars.com, TrueCar, Carvana, Hemmings, Cars and Bids, Car Soup, Cars Direct

They also provide external links AutoTrader, CarGurus, Facebook Marketplace and Craiglist

cars.com – They offer private classified ads but most results will be sourced from local dealers and online sellers Carvana, Shift and vroom

TrueCar – They are an aggregator of local dealers and online dealers, including Carvana and vroom

Ebay – Not an aggregator, but may include listings from private parties as well as physical dealers and online dealers

Autotrader – They offer private classified ads but most results will be from local dealers

Cargurus – They offer private classified ads but must results will be from local and online dealers; includes CarMax and shift

Carvana – Primary source where they sell cars they have purchased. Online-only, no-haggle.

In the last couple of years I’ve bid on at least 5 different online auction sites and purchased cars on 3 of those. Here is my experience.

Ebay

I bought a car from Ebay Motors in February 2020.

Research

Auctions are up for days so plenty of time to research the VIN

You can ask the seller questions privately

The pictures are often limited and not of great quality

There isn’t much transparency in terms of the listing – there are no standards in terms of what a seller must include or not include in their description.

There is no chat or commenting system with input from other enthusiasts

Bidding Process

Proxy Bidding – You enter the most you’re willing to pay. Ebay will automatically bid for you to the highest amount not exceeding your max bid. If your max bid is higher than the next highest max bid, the price will immediately jump to just over the next highest max bid. If your max bid is not the highest, it’ll be bid up to over your max bid.

No deposit is required to bid

Winning

It is my understanding that even if you win the bid you aren’t actually obligated to complete the transaction although most sellers demand some form of down-payment immediately following the auction. This could allow a purchase inspection to complete before agreeing to complete the transaction.

In my case I bought a car less than 100 miles away so went to see it in person

You’re buying from an individual yet Ebay didn’t have any kind of assistance for purchasing like an Escrow service. I tried to convince seller to use escrow.com but he refused. I ended up wiring the money which meant the seller had both my funds and the vehicle before he released it to me, which made me very nervous and then of course you need the seller to transfer the title.

If I were to do this again I’d insist on using an escrow service. It looks like since 2020 Ebay has partnered more deeply with escrow.com

Taking Delivery

It is between you and the seller to arrange shipping. In my case I purchased Hagerty insurance then immediately used their free towing since the vehicle was close by

BAT or Cars and Bids

I bought a car from BAT in November 2021. I have not bought a car from C&B. However they are so similar, I’ll group them together.

In the listing for the car I bought a number of flaws were mentioned. However, there were a significant number of additional flaws that were never mentioned. Radio doesn’t work, some parts of digital dash don’t work, power antenna doesn’t work, broken window moulding. Fuel gauge was described as “intermittent” but it is basically non-functional. Smokers car, no key for the t-tops. Shows the risks of purchasing basically sight unseen. Photos can hide a lot.

Research

Auctions are up for at least a week so allows as much time as you need to research the VIN, ask questions and review other commenters feedback

There are typically hundreds of photos and often videos posted

On BAT for popular cars there are typically very knowledgeable commenters on the thread

I like the fact on Cars & Bids there is a “Known Flaws” section. BAT doesn’t have this and any flaws are either mentioned in the narrative – or in fact not at all.

Bidding

Neither site uses proxy bidding. The amount you bid is exactly the amount the sales prices jumps to. You of course have to place a bid higher than the current bid.

Both sites take a deposit on your first bid

Down to the final 2 minutes, each new bid resets the clock to 2 minutes to prevent sniping

Winning

When you win, negotiating the payment, title and delivery is between you and the private seller

BAT sends an email with a receipt for the buyers fee

I asked the seller to send a photo of the title then wired the money

He put the title in the mail and sent me a tracking number

Delivery

BAT provides a handy shipping quote option. I found the quotes to be cost-competitive with shipper on U-Ship however… it said that pickup would be within 10-14 days which seems awfully long. Most shippers pick up between 3 and 5 days.

The seller ended up providing a shipper who charged two-thirds of BAT

Costs

A 5% buyers fee is charged and a hold is placed on Credit Card as soon as you bid

GAA Auctions

I bid on some cars on GAA but have never purchased. Some key points:

GAA out-sources actually bidding process to a system called Proxibid.

Proxibid has a ton of features, even though the design isn’t that modern

You can place a proxy bid in advance of any auction. It shows the current high bid just like Ebay

Cars are only sold when they roll across the auction block and there is live bidding

You can watch the live stream of bidding, although in one case this failed to work. Its unclear what the audio/video lag is

Like every auction other than BAT and C&B, opportunities to research are very limited, listings are sparse

The hammer price was $12,000 but they add the 10% buyers commission when the quote the sales price – although online I had to pay 12% which was not reflected in the price.

Its a bit of an odd truck – looks pretty straight but claims to have a 327 CI engine which if true means someone swapped in a Chevy engine. From research, it has a New Process 435 manual transmission which seems to bolt up to almost anything, so this all seems plausible. I’m curious to learn what era the 327 came from.

I used classic.com to research this vehicle and found it may have been sold at auction in 2014, 2015 and online in 2019. If the 2014 link is correct, that listing claimed a 390 CI engine and a “Recent restoration”. The 2015 sales doesn’t mention the engine size. The potential 2019 sale (determined by the date at which the walkaround video was uploaded to Youtube) also doesn’t mention this.

Research

From a research perspective, listings on Mecum offer _very_ few details, not even a VIN until close to the auction. In my case there was no VIN until they posted a walk-around video something like 8 hours before the auction and I had to transcribe the VIN from the video

There is zero opportunity to ask clarifying questions and obviously no commenting or feedback

So unless you’re present at the auction and have had a chance to personally view the vehicle, from an online perspective you basically buying sight-unseen (or at least only seeing a handful of pictures of varying quality and one un-narrated walkaround video)

Bidding

You can enter a proxy bid for the most you’re willing to pay and Mecum will bid for you to that amount. Similar to Ebay. That is how I won my auction. Unlike GAA, Mecum does not show other people’s proxy bids, only your top bid, but its not really an issue since being the top proxy bidder doesn’t really have much of a bearing on the auction itself.

Cars are only sold when they roll across the auction block and there is live bidding

You can also manually bid if you didn’t provide a proxy bid or if it has been exceeded

The Mecum bidding page allows you to watch the bidding video stream live and follow-along in the bidding process and manually bid. On a desktop browser, there is very little lag. I’d strongly recommend watching the live stream for auctions you’re bidding on on desktop only, not mobile, where there is likely to be a ton of lag.

It is super fast-paced and does fairly well transition between in-person bids and internet bids

As far as I can tell you can only bid online with the next ask prices the auctioneer sets. For example if a vehicle is bid to $20k, the next price to bid online might be $22k, you cannot offer $21k for example

Winning

Once you’ve won there is no way to initiate payment online, you have to wait for them to send an invoice.

The invoice is payable immediately upon receipt. Included the hammer price, the 12% buyers fee, an $85 other fee (some kind of documentation, I think) and Tax at 6.25% which is Illinois used car tax

You are paying Mecum directly. I set up a wire but since I did so on a Saturday, it would take until Monday to clear

Delivery

Mecum require vehicles to be picked up by 3pm Monday. I used U-ship to generate transportation bids. Bids were in the $1200-$1600 range to ship Open Transport from Illinois to California. But almost no-one could commit to picking up in that small time window only in a multi-day range. Having had a bad experience in the past, and given that I would be traveling on vacation Monday, it felt like a lot could go wrong here trying to organize a shipper to pick up in a very narrow time window.

I requested a quote from Mecum’s Auto Transport service. They quoted $3,000 for a closed transport option. Unfortunately they had no cheaper open transport option. However, the kicker here is they take care of everything. I ended up going this route because I would not be available to deal with coordination of an external shipper.

I paid by credit card and they charged me an 3.5% fee for $105 🙁

Good news is immediately upon payment I get a link to a shipment tracker, so its all good to go

They told me it would take 10 to 14 days to arrive, which seems like a lot longer than other shippers but since I’m on vacation for a week, that actually works for me

Update on shipping

Reviewing the online tracker, it wasn’t picked up until Wednesday

I got a call on the Friday (6 days later) that the truck would be delivered Monday

I then got a call on Saturday (next day) that the truck had broken down

I spoke to the driver Monday and he said he’d need another couple of days to figure out how to get it to me

I think it was Thursday by the time they got it on another truck

Truck was delivered Saturday (a full 2 weeks after purchase)

Costs

To register with Mecum Chicago 2021 it cost me $200. There is a more expensive option that seems geared to people in-person

That gave me a bidding allowance of $50k without having to do any funds verification.

It gives you access to some different views, one of which is just a giant list of all the auction lots that update in realtime as they are bid and won.

It gives you access to the live auction page and a non-delayed video stream (unregistered video streams are delayed 30 seconds)

I was watching the auction but thought the price had exceeded my proxy bid, but when I heard the auctioneer say sold on the internet for $12k, I realize I had won.

Internet buyers pay a 12% commission on winning bids. When they update the sold prices on their listing, they include the commission.

Summary

Auction Registration – $200

Hammer price: $12,000

Internet buyers fee of 12%: $1,440

Doc fee: $85

CA Sales Tax is going to be $980.56 (of which I already paid 6.25% to IL)

Shipping: $3k

Shipping CC charge: $105

CA Title & Reg: Unknown

So my $12k auction purchase actually cost me $17,700 to buy, ship and pay taxes. Ooof.

Lessons learned:

Mentally add 12% to your final price for your purchase cost

Note that shipping will add a significant chunk to the costs especially since using Mecum’s closed transport option seems like the only hassle-free way to do this. So consider purchasing from much closer auctions, or if you’re buying a driver, be prepared to pick it up yourself and drive it off – but recognizing this won’t be until the first business day following the auction if you’re wiring money. Presumably if you write a check-in person or drop a bag of cash you can take it immediately.

Summary

Ebay is proxy bidding only, free to bid and a transaction between private parties

Up to you to title / register at your DMV, pay taxes etc.

BAT and Cars and Bids are live bidding only, refundable deposit to bid and a transaction between private parties

Up to you to title / register at your DMV, pay taxes etc.

GAA and Mecum are proxy bidding plus live bidding.

Mecum charges $200 to “enter” the auction; Mecum charges 12% and purchase transaction is between you and Mecum and so they will withhold local tax that you can credit against your own state’s tac

I made the decision to purchase solar. With a pool pump and solar pool heating and A/C my electric bill has climbed substantially.

There is a world where I may plan to move in about 12 months so debated whether to move forward with solar. There are some studies that suggest owned solar will increase the value of a home. https://www.zillow.com/research/solar-panels-house-sell-more-23798/ I’d only need the value to increase by 1-2% to recoup the costs. I went for it.

My usage

Average Electric Usage per month over the last 12 months – 714 kWh with average total electric charges of $214 (includes delivery, generation, bonds, taxes and fees).

Total is 8568 kWh for the last 12 months (Important for later)

Bill Period

Total Electric Usage

Avg. kWh/day

Total Electric Charges

Avg. $/Day

Average Cost

11/9/20

800

25

$251.77

$7.87

$0.31

10/8/20

868

29.93

$277.77

$9.58

$0.32

9/9/20

1010

32.58

$293.00

$9.45

$0.29

8/9/20

854

27.55

$238.76

$7.70

$0.28

7/9/20

730

24.33

$228.79

$7.63

$0.31

6/9/20

724

24.13

$219.85

$7.33

$0.30

5/10/20

660

20.63

$193.64

$6.05

$0.29

4/8/20

537

18.52

$159.90

$5.51

$0.30

3/10/20

548

18.27

$164.71

$5.49

$0.30

2/9/20

575

18.55

$168.56

$5.44

$0.29

1/9/20

598

19.29

$178.46

$5.76

$0.30

12/9/19

663

20.72

$202.45

$6.33

$0.31

Average

714

$214.81

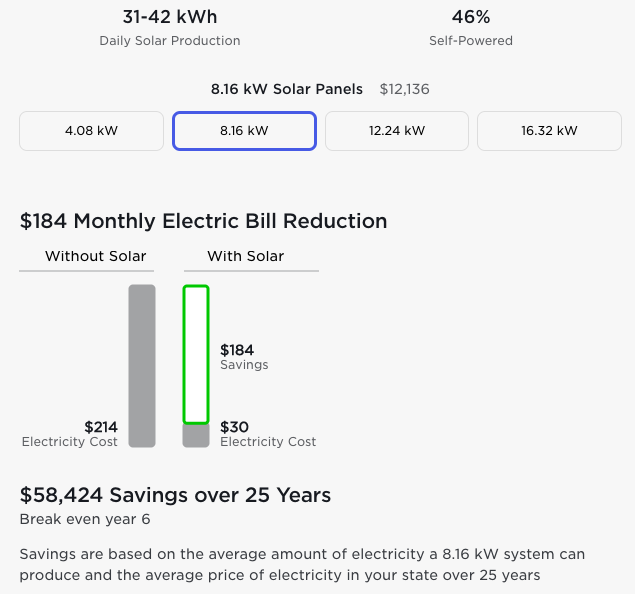

Using the Tesla Solar calculator for my home address and an average electricity bill of $214 Tesla indicates I need 8.16 kW panels but that will only cover $184 of my bill.

This doesn’t compute with other solar quotes or Project Sunroof. Project Sunroof indicates for a $200 average electric bill a 4.8 kW system will cover 100% of my electric bill.

Using EnergySage solar companies are quoting 5 – 6 kW systems to cover my energy usage.

Using pvwatts default settings for my location suggests a 5.3 kW system will cover my annual electric needs.

However, since Tesla solar was price competitive I decided to proceed and figure it out late.

Sunday Nov 1st – Order online

I initiated the process and complete the process of taking photos of my roof, electrical panel etc. this included reviewing a design that showed the 24 panels (340W each). Sixteen panels on the south-facing roof slope and 4 panels each on west and east facing slopes. These are mounted below my solar pool heating. I’m unsure if it is wise to install electric solar below a water solar system.

Friday Nov 6th – Checking in

Texted to ask what next steps are. Rep indicated permits were submitted on November 2nd with an estimated timeline of 5-7 business days. I was given a number to call to schedule a home assessment, which I did although my earliest availability was November 19th.

Cumulative time: 5 days

Wednesday Nov 11th – Received update

Rep texted me to indicate permits were submitted. Meanwhile… I wanted to query the system sizing.

Texting with rep she indicated the 8.16 kW system for my house would generate an average of 1023 kWh per month. This is 43% more than what I actually need.

The only thing I can think is that their calculator is using a cost per kWh much lower than my actual costs. Do they consider baseline usage? Summer versus winter charges? TOU costs?

By my calculations I can cover 100% of my electric needs on average with 16.5 panels. Since I can get 16 panels on the south-facing portion of my roof that seems like a sensible approach.

Thursday Nov 19th 2020 – Home Assessment

Spoke to the assessor and queried the system sizing and the location of the panels. I indicated I’d prefer to simply have 16 panels on the south-facing portion of my roof and forgo the other 8 panels on the east and west portions. He agreed to record this on his assessment.

I know my electrical panel will need upgrading. It is original to the 1979 portion of the house, is 100 amp and totally full. I asked about that and he said engineers would review.

I won’t count the time it took me to schedule the assessment as elapsed time.

Saturday Nov 21 – Check in

The status had not changed on my account, so I queried my customer support rep to ask for next steps. She indicated waiting on permitting (although I thought that was done?). Did not indicate anything about the electrical panel.

I also mentioned my HOA Architectural Review Board. As part of the intiail process they asked for the name of the HOA but did not ask for any contact details.

Cumulative time: 7 days

Tuesday Nov 24 – Received blueprints

Received blueprints for system. Updates for the 16 panels on the south-facing portion of roof only for a 5.44 kW array. I’m asked to submit to my HOA architectural review board and email Tesla when permit is received, however I’m not expecting this to block installation date.

I texted again to ask about electrical panel and any upgrades and costs associated with that.

The design indicates Tesla’s estimate for system production: 8832 kWh. This is in excess of my actual last 12 months electricity consumption. I’m comfortable, then with my decision to downsize to 16 panels. It begs the question what Tesla are doing on their website estimator to suggest that a much larger system would only cover a small portion of my bill.

Wednesday Nov 25 – Received new document notification

I received a document indicating the roof was not suitable as-is for installation. I don’t get a specific reason but a list of possible reasons. It includes a $5,280 pre-construction cost to re-roof the portion on which the solar panels will be installed.

I queried whether there were going to be any other pre-construction costs, such as electrical work. The rep indicated she would get back to me.

Cumulative time: 11 days

Monday November 30th – Received multiple notifications to review documents

Receiving reminders to review and sign the layout and pre-construction documents. I queried the rep again to ask if there would be any more pre-construction costs, I do not want to sign up for work without knowing the full costs.

The next day the rep indicated there was no other pre-construction work. I signaled my surprise since I’d been told previously I would need an electrical panel upgrade to install solar and since then I’d had A/C installed which required some hoop jumping and re-purposing of a disused electrical dryer circuit.

The next day (December 2nd) the rep said she would review with Project Management team.

I’m going to count this time since I have open questions I am waiting for response for.

Cumulative time: 16 days

Monday December 7th – Queried rep again

I’d received multiple notifications to review my documents but since I was expecting a response on the electrical panel I took no action. So I queried the rep again to find out when I’d get an answer.

Same day she replied and indicated that they can move forward with my current electrical panel.

Cumulative time: 23 days

Saturday December 12th – Decided to proceed

I decided to move forward. While the partial re-roof was an unfortunate additional expense, with the smaller system, the total costs were still in-line with what I had originally budgeted.

I signed the documents.

Soon afterward the website updated to indicate:

Installation: Coming Soon

We’ll reach out to you when your installation is ready for scheduling.

I won’t count the time it took me to make a decision.

Cumulative time: 23 days

Monday December 21st – Queried when installation would be scheduled

Since I hadn’t heard anything I queried the rep to ask when I could expect to be contacted or how far out installation was running. She told me she could not tell me anything about installation and I would be contacted “once approval is received to move forward”.

Cumulative time: 32 days

Tuesday December 29th – Queried again

I asked again when I’d get an update on approval to move forward and contact from scheduling team. The rep said she would look into it.

Cumulative time: 40 days

Checkpoint

So far almost 2 months in and 40 days of time spent on the Tesla side.

It really only took 11 days (not counting time to schedule Home Assessment) to get to documents.

However it took 12 days to get to a final answer on the electrical panel.

It has now taken 17 days since I signed and no installation scheduled (Christmas period in there, but I imagine only a couple of days off?)

Tuesday December 29th – Roofing Update

Coincidentally I received an email from a project coordinator on the roofing team, copying in a roofing contractor in my area indicating

you can be expecting word from our scheduling department to help coordinate your construction schedule within the next 5 business days.

You will also be contacted by a representative of ACCI Roofing, to discuss the specifics of your re-roof

Thursday January 7th – Queried

I waited a full 9 days (it was over New Years) but did not receiving any contact from the scheduling department. I sent an email.

I did receive a reply same day indicating someone from the roofing contractor will contact me to schedule and the installation would be scheduled following that.

Cumulative Time: 49 days

Wednesday January 13th – Roofing Contract

Finally 15 days after receiving the Tesla email I received an email from the roofing contractor with a contract to sign indicating that their schedule is 4-6 weeks out. I had a question about the tile selection since this is a partial re-roof.

Cumulative Time: 55 days

Thursday January 14th – Queried

Responded to roofing contractor email with questions about tile selection / color matching.

Wednesday January 20th – Roofing Scheduled

Emailed follow-up to roofing contractor. They called back and explained that they don’t actually replace the tile, rather prepare the roof, flashing, put down shingles and then once solar is installed place the original tile around the solar installation.

Contractor indicate they had a short-term availability and could come next day which I accepted.

It basically took 22 days from the Tesla email to scheduling the re-roof. If they didn’t have the short-term opening, I might have been waiting another 4-6 weeks.

Thursday January 21st – Roofing Project

Roofing contractor came and did the partial-re-roof.

Following that I emailed Tesla roofing project manager to query when they’d schedule installation.

Friday January 22nd – Install Scheduled

Received a call from Tesla scheduling indicating they had an opening tomorrow. Since the weather was showing an 80% chance of rain I asked what would happen if it rained. The person indicated they’d still come out and attempt to install as much as possible or would reschedule hopefully within the next couple of weeks. Seems like a bit of a risk to try to bring the installation in by 4 days for it potentially to be delayed by a couple of weeks. Decided to take the risk and accepted that opening.

Later in the day I received a text from my usual rep indicating due to potential for rain, they’d reverted to my original installation date of Wednesday 27th…

And then on the 25th they called me to say they could do it on the 26th…

Cumulative Time: 54 days

Tuesday January 26th – Install

Tesla team installed the panels and system. They were here for about 6 hours. I later received an email that inspection was scheduled for tomorrow.

Wednesday January 27th – Inspection

System was inspected and passed. I received a note that final payment for the system was due. I paid from my bank account.

Instruction was that I should receive contact from my electricity provider (SDG&E) within 10-12 days for approval to turn on. Reading SDG&E website indicates that it could take 5 business days for permission to operate. They mention a fast-track process but I don’t know if that was followed or how “fast” fast-track is.

I also emailed roofing contractor to ask for next steps for finishing the roof.

Cumulative Time: 59 days; Calendar elapsed Time: 88 days

Friday January 29th – Receive PTO

Received an email with Permissions To Operate from Sempra Engergy (owner of SDG&E).

I went outside to flip it on. Panel breaker was already on, the disconnect was already on, turned on the inverter.

The website “how to” indicates it could take up to an hour to see data in the app. However, am concerned that the gateway box is too far from my inverter to work.

Data was not showing up. I texted my Tesla rep to find out if I needed to do anything but all I received were instructions to turn the system on. I rebooted my gateway box. A few hours later once the website changed to indicate it was time for me to download the app, the data began to show up. So I do think Tesla had to enable something on their side.

Cumulative Time: 61 days; Calendar elapsed Time: 90 days